Top financial institutions have rallied behind a new report calling for the government to accelerate the digitalisation of UK markets to deliver a £33bn annaul boost to the economy.

The paper, backed by a 54-strong taskforce that includes the likes of Barclays, JP Morgan and Lloyds Banking Group, says the tokenisation of markets could add hundreds of billions of pounds of economic value to the UK over the next decade.

Tokenisation refers to the digital representation of asset ownership on a blockchain, which stores data across a decentralised network of computers. Trading assets as a token is seen as a way to increase speed and slash administrative cost and burdens by replacing market infrastructure with automated software.

Chris Woolward, who was appointed the wholesale digital markets champion earlier this year, led the findings and set out a 12-month plan covering nine key areas to harness the technology.

“Tokensided markets offer a significant opportunity to the UK in terms of efficiency and the potential for innovation and to defend our global position in the established markets,” the report says.

It adds if “implemented at scale” tokenisation has the potential to free up capital for growth and strengthen the UK’s competitive standing.

City urges faster progress

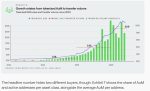

The report estimates the global market for tokenised assets could reach up to $88tn by 2035.

Estimates from Barclays and PwC suggest this uptake globally could generate a £33bn increase in the UK’s economic output and generate an extra £14bn in taxes.

Miles Celic, chief executive of TheCityUK, said global competition was “fierce and intensifying,” calling for the UK to be “much faster, more ambitious and more creative” to stay ahead.

“There is no automatic right to success,” he added.

The report warns there is strong competition across digital markets from the dominance of the US, as well as a growing presence in the United Arab Emirates, Singapore and Hong Kong.

“A lack of pace would bring fundamental risks to the UK’s influential position as a global leading financial services hub,” it says.

Chris Hayward, policy chairman of the City of London Corporation, said the UK could lead a “digital big bang in financial services” if it accelerates the “adoption of tokenisation”.

Regulation around digital assets has become a topic of fierce contention in the last year. The Bank of England eventually watered down the final version of its rules for stablecoin.

The Bank’s governor Andrew Bailey was previously accused of “killing” the country’s stablecoin ambitions with “prescriptive” views.

He has also been on the receiving end of criticism from Reform UK’s Nigel Farage, who branded him a “dinosaur” for his rhetoric around cryptocurrency.

In the central bank’s final framework for stablecoins, it ditched plans to impose a limit on customer deposits and instead impose a temporary cap on the total volume of sterling-denominated tokens in circulation.

+ There are no comments

Add yours