| Updated:

While much of the media obsesses over Nigel Farage’s fight with a man dressed as a bin, I have something more sobering to discuss as we kick off the weekend.

The Office for Budget Responsibility’s report into fiscal risks and sustainability, published this week, is comfortably the most alarming yet. This is an annual review looking at the dangers facing the UK over the next half-century.

However you look at it, our public finances are deteriorating rapidly, and unless action is taken, we could wind up in a car-crash situation.

‘Unsustainable and ever-rising’

“In nearly all of the scenarios we explore, debt eventually moves onto an unsustainable and ever-rising path,” the OBR writes, in one of dozens of damning verdicts over the way successive governments have managed the economy.

I’ll spare you having to go through each one in turn, but I do want to highlight four charts from the report which powerfully illustrate the sheer scale of the challenge facing the UK.

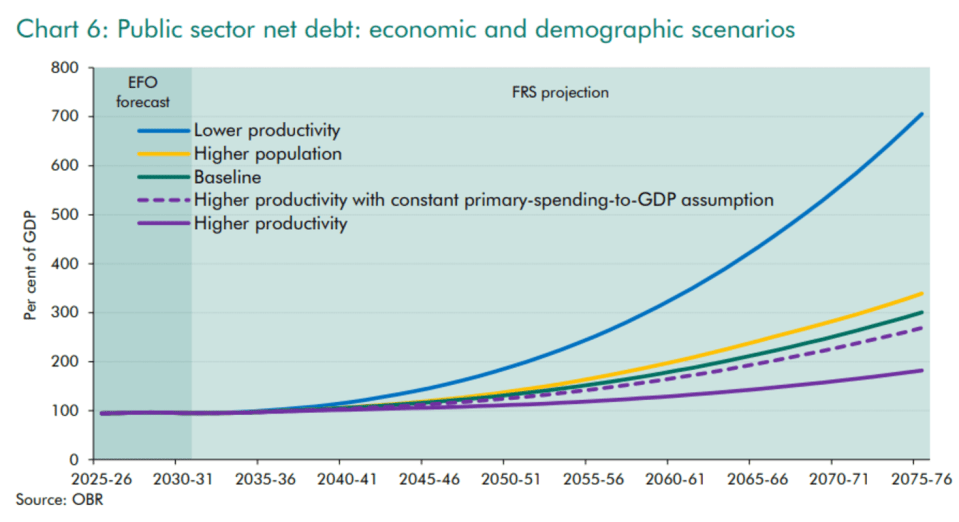

The first is the most straightforward illustration of the problem. Based on current trends, public sector net debt (PSND) is set to swell from the roughly 100 per cent of GDP it is now to as much as 300 per cent by 2075. That is a truly staggering figure and the government could well see its ability to borrow wiped out long before we get there.

That projection is based on certain assumptions the OBR has made about productivity improving. If it doesn’t improve, PSND could swell to an eyewatering 700 per cent of GDP. Even in a best-case scenario, where more productivity gains are made than the OBR predicts, debt will still swell to 180 per cent of GDP. That is the best-case scenario.

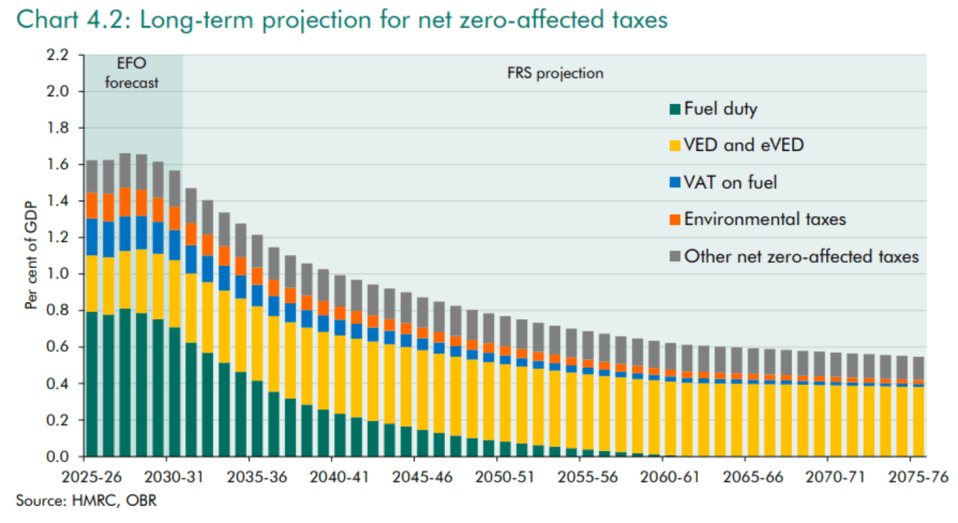

The second chart looks at the effect of our net-zero transition on the tax base. It shows that as we move towards electric vehicles and renewable energy, the receipts from fuel duty and other environmental taxes will evaporate, with revenue raised from net zero-affected taxes tumbling from 1.6 per cent of GDP today to 0.5 per cent by 2075.

Longstanding taxes are rapidly diminishing in their importance to the exchequer. That in part explains why the government has been scrambling to raise tax rates and find fresh things to tax over the past couple of years. That pattern, unfortunately for us taxpayers, is unlikely to change.

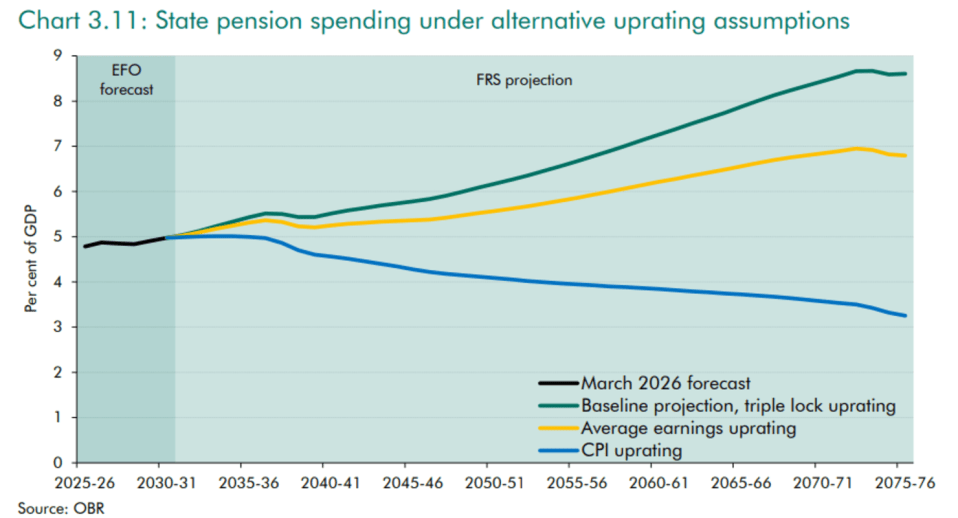

The third looks at the single-biggest policy burden on our public finances: the triple lock. This is the commitment by governments to ensure that the state pension rises in step with inflation, wages or 2.5 per cent each year. It’s a policy that effectively guarantees that welfare spending will grow faster than the economy grows, every year, forever.

It is no overstatement to say that unless this policy is dropped, the British government will eventually morph into a giant pensions pot which also serves a few basic functions on the side, such as policing and defence. The OBR chart illustrates this.

The level of spend on the state pension will almost double as a share of GDP, from five per cent to nine per cent, over the next 50 years if the triple lock stays in place. If we instead transition to a much more sensible policy of linking pensions to inflation, spending will instead fall to a more manageable level of three per cent.

The root cause

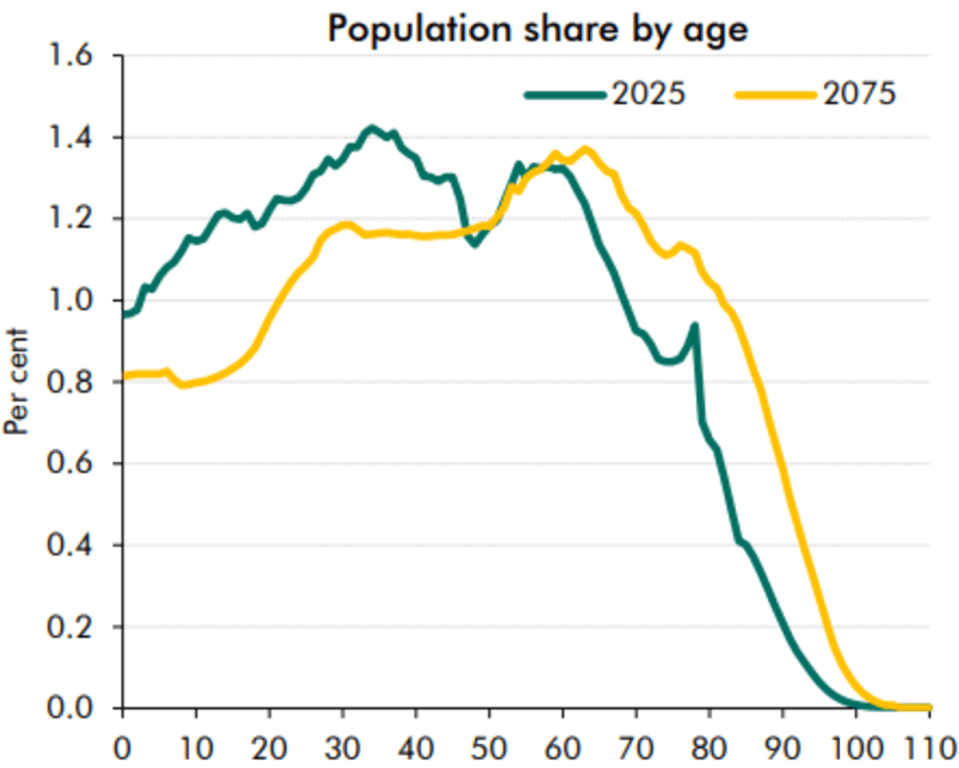

The fourth captures why the danger is set to escalate, year after year: our population is rapidly ageing. Historically this has been because advances in medicine have allowed people to live longer, but over the next half-century, the primary driver will be the relative paucity of young people: couples are having fewer children.

This is a double-edged sword because not only are older people greater net consumers of state resources, but fewer young people will mean fewer net-contributors when they get jobs. In other words, we won’t have enough people in the workforce to pay for it all.

We are not yet at crisis point, however. The OBR points out that taking immediate action to reduce the deficit would make our future demographic and economic changes much more manageable, massively reducing the costs of servicing debt by both bringing down overall debt levels as well as reducing interest costs. If this is taken seriously, we might just pull through.

But do you trust the government to show the maturity needed to get ahead of this problem? Given our future PM, Andy Burnham, has already recommitted Labour to the triple lock, I’m preparing for the worst.

+ There are no comments

Add yours